Exploring the Concept of Religion and Film

May 30, 2023

Strategic information system

May 30, 2023

Introduction

When operating a business, making correct decisions can result in success, on the other hand, making wrong attempts and things in business can lead to failure. With various decisions to make, it is very important to put every aspect of the business into consideration for an effective business outcome. To help the individuals in making effective efforts for such measures, the leaders of the organization need to go through a very intricate and thoughtful decision-making process (Ammann, Oesch & Schmid, 2013).

As per Andreou, Louca & Panayides, there are various methods and techniques which help the organization in making good and effective decision-making. These tools and techniques may tend to encompass similar major principles of reasoning out the decisions which are required to be made, researching and considering the choices, and making a review of the decision after it is been (Andreou, Louca & Panayides, 2014). Capital budgeting can be considered as planning that is for a long-term basis that is meant for the commitment of various funds for fixed assets. To evaluate long-term planning, the managers in the finance department make use of the following techniques such as net terminal value and internal rate of return. The parameter of the assumptions and values of any kind of model that are used for the decision-making of an organization are subject to error and change (Aribi & Arun, 2015).

Sensitivity analysis

As per Arnold, Sensitivity analysis can be broadly defined as the investigation of such potential changes or alterations that occur in the organization. It also encompasses the impacts of such changes and errors on the outcomes that are to be drawn. Sensitivity analysis can be easily implemented by companies in the case of their decision-making process. It is very easy to communicate even. It is the most useful and widely used technique that is available to the modelers who support the decision-makers in the companies (Arnold, 2013). It is to be noted that stability and sensitivity analysis has to be an integral part of the decision-making and resolution strategy. There is a broad range of applications to which sensitivity analysis is applied (Aussenegg, Goetz & Jelic, 2015).

Figure 1: Sensitivity Analysis

The economic and financial benefit of cost analysis on the projects that are in the investment kind of nature of the companies is based done the quantifiable variables forecast. Sensitivity analysis concentrates on the analysis of the implications of the changes in the major variables in the IRR and NPV of the projects which involve many instances of decision making. It is observed that a project or decision-making of the company having a higher variability is high in risk. This happens because the investors need a higher rate of return times when the companies undertake projects that are high in risk, such companies will have greater capital costs (Baños-Caballero, García-Teruel & Martínez-Solano, 2014).

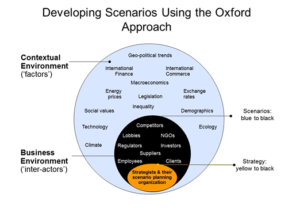

Scenario Analysis

According to Chen, Han & Zeng, The sensitivity and scenario analysis of any business venture can be obtained by analyzing the internal rate of return along with the standard deviation as an outcome of the volatility of the cash flows that are expected. The economic and financial benefits of the cost analysis of the investment projects are determined by the forecast of the quantifiable variables (Chen, Han & Zeng, 2015). The values of such variables are assumed based on the most predictable forecasts that encompass a longer period. The value of such variables for the most likely values may vary from the values that are forecasted considerably based on developments in the future. This can be done using sensitivity analysis (Deakin, 2017).

Figure 2: Scenarios Analysis

The variability of the decision-making in the projects in the companies is evaluated based on the comparison of the internal rate of return (IRR) which includes EIRR and FIRR to the economic or financial opportunity capital cost. The decision-making in the project, alternatively is considered to be viable when the NPV which is the Net Present Value is positive. By using the selected OFCC or EOCC as the rate of discount, sensitivity analysis concentrates on the analysis of the implications of the alterations in the major variables in the IRR or NPV of the decision-making in the projects undertaken by the companies (Jain, 2017).

A review of the evaluation and literature of reports presents a very commonly found fact that the assessments of these values do not facilitate sufficient information for a decision that is valid, especially for investment projects in the public sector domain in environments that are highly uncertain like in developing countries. Analysis of the risks cannot be considered as a substitute of the conventional methodology for the investments appraisal, however, a technique for the improvements of the results (Kovářík & Sarga, 2014). The sensitivity analysis of the investment projects by the companies and their evaluation is embedded in a constantly altering environment which exerts impacts on the predictions and values of the analysis of the risks. The objective of such analysis is the identification of such variables that sensitively react to external changes at a greater rate, which ultimately results in changes in NPV and IRT. The external changes have implications on specific input values such as criteria values like NPV and IRR of the evaluation of the projects (Le & Ngo, 2016).

NPV calculations are sensitive to the influence of the external environment like interest rates, inflation, currency exchange rates, and economic growth. To evaluate the NPV of any business project, the managers in the companies are faced with a single rate of discount and multiple periods of cash flows. According to Le & Ngo, it can be stated that decisions are determined by cash flows, and financing costs are not considered in the analysis of cash flows. Hence, financing costs are included in the decision-making process of the companies through the needed return rate (Le & Ngo, 2016).

On the other hand, the net present value which is the NPV is the difference between the current value of the cash inflows and the current value of the cash outflows. If through the scenario analysis, the probability of the distribution of all the variables is analyzed. Scenario analysis begins with the construction of the fundamental scenario of the case. Other scenarios are considered from there which are considered as “best and worst case scenarios” (Liu, 2014).

Source: (Liu & Huang, 2016)

Through scenario analysis, probabilities are assigned to various scenarios and calculated to converge them at a value that is expected.

Bren Even Analysis

A break-even analysis will frequently convert the crucial variable of business projects of a company which is the volume of sales. If any company thinks of designing and launching a new product or service, break-even analyses assist in predicting how well it can be sold (Ojo, 2016). Break-even analysis is the most common and widely used tool that can be used for analyzing the association between profitability and volume of sales. Forecasting risk is probable regarding the aspect of what will break or make the expansion of any business projects to any company in terms of the volume of the sales.

Based on the estimated flow of cash, the expansion in the business of any company has a positive effect on NPV. To have a financial break even, the level of sales has to be zero. For simulation analysis, a computer is used to generate thousands of probable scenarios in the case of expansion of the business of a company (Ortas, Gallego‐Alvarez & Álvarez Etxeberria, 2015). The distribution of probability is assigned to every combination of the variables to create a complete range of potential results. Simulation can be considered as the imitation of the conduction of a system or process which is real in the world.

Simulation Analysis

The simulation analysis includes the behavior of the system which is generated by the system’s artificial history through the utilization of random numbers. Companies make use of the simulation analysis for building the models of how varying the courses of external variables and courses of action may influence the building models, and finances which allows the companies for reacting quickly with a prepared plan (Wang & Sarkis, 2013). Developing and initiating the forecast of the business plan would include the forecasted statement of income, both the variable and fixed costs that have a significant effect on the NPV and IRR. Simulation analysis assists in changing the income of the company as a whole as the basis of the volume of sales. Alterations in the expenses that are based on the potential alterations to both the variable and fixed costs affect the IRR and NPV.

Simulation analysis projects the alterations to the expenses and revenues without considering the possible cause of them. It states the impact on the IRR and NPV when the variables of expense and income are put into adjustments. This helps the business organization in its decision-making process of the organization as it maintains the viability of the company to keep the business open for the entire duration of the business operation (Ortas, Gallego‐Alvarez & Álvarez Etxeberria, 2015).

Recommendation and conclusion

One of the most crucial factors which affect the investment project of a company is the internal rate of return which should be higher than the rate of return that is acceptable to the actual rate of interest of long-term available loans in the market. Hence, to justify the plan of the investment projects of the companies, some individuals try to implement different methods and present an internal rate of return that is higher than the actual one. Thus, they devise many unrealistic numbers and raise or reduce some of the numbers that alter the internal rate of return, which is the increase in the company’s sales that are presented in various cases to present the justification of the project.

The next aspect that has a significant effect on most of the investment projects of companies is the minimization of the schedule of the plan of the investment projects of the business by altering it and unrealistically presenting, the internal rate of return changes. However, the issues that are considered regarding the actual time of the investment project of the business organizations have the potential to make them unjustified. Another factor that has a significant role in the success of the business projects of the companies is the NPV which when positive, will present that the investment projects of the business organizations are justified. By the research analysis and study that are conducted, the factors that are effective in the rise of the NPV, are the decrease of the rate of discount and in some instances increase in the company’s sales.

This also encompasses the presentation of the business plan is justified, some companies reduce the rate of discount in a very unrealistic manner or make a hike in the sales of the companies to present the Net Profit Value to be high. To prevent these types of cases, the information regarding the investment projects of the business organizations must be very intricately examined and assessed carefully. The sensitivity analysis needs to be examined from various perspectives by reality in an exact manner.

The revenues of the investment project have to be regulated along with being considered as its decrease or increase has significant implications on the justification of the investment projects of the companies. One of the key factors that are to be kept into consideration is the schedule of time. If the time of operation of the business projects decreases, it can raise the justification of the business project and vice versa. Hence, the exact schedule of any business project is very crucial. The exchange type and the cost of investments in the business operations are very significant aspects that are to be considered regarding the overall sales of the company. These aspects, however, relate to the effectiveness of the fluctuations of the rate of exchange on the feasibility of the business projects.

References

Ammann, M., Oesch, D. and Schmid, M.M., 2013. Product market competition, corporate governance, and firm value: Evidence from the EU area. European Financial Management, 19(3), pp.452-469.

Andreou, P.C., Louca, C. and Panayides, P.M., 2014. Corporate governance, financial management decisions, and firm performance: Evidence from the maritime industry. Transportation Research Part E: Logistics and Transportation Review, 63, pp.59-78.

Aribi, Z.A. and Arun, T., 2015. Corporate social responsibility and Islamic financial institutions (IFIs): Management perceptions from IFIs in Bahrain. Journal of Business Ethics, 129(4), pp.785-794.

Arnold, G., 2013. Corporate financial management. Pearson Higher Ed.

Aussenegg, W., Goetz, L. and Jelic, R., 2015. Common Factors in the Performance of European Corporate Bonds–Evidence Before and After the Financial Crisis. European Financial Management, 21(2), pp.265-308.

Baños-Caballero, S., García-Teruel, P.J. and Martínez-Solano, P., 2014. Working capital management, corporate performance, and financial constraints. Journal of Business Research, 67(3), pp.332-338.

Chen, Z., Han, B. and Zeng, Y., 2015. Does Corporate Financial Risk Management Add Value? Evidence from Cross-Border Mergers and Acquisitions.

Deakin, M., 2017. Property management: corporate strategies, financial instruments, and the urban environment. Routledge.

Jain, A.K., 2017. RATIONALITY, BEHAVIOURAL ECONOMICS, AND CORPORATE GOVERNANCE. Journal of Financial Management, 1(1).

Kovářík, M. and Sarga, L., 2014. Implementing control charts to corporate financial management. WSEAS Transactions on Mathematics.

Le, N. and Ngo, P.T., 2016. Local bank access, financial flexibility, and corporate liquidity management.

Liu, A.Z., 2014. Can external monitoring affect corporate financial reporting and disclosure? Evidence from earnings and expectations management. Accounting Horizons, 28(3), pp.529-559.

Liu, J. and Huang, L., 2016. The New Era of Corporate Financial Risk Management and Control Strategy Research. DEStech Transactions on Social Science, Education and Human Science, (helmet).

Ojo, A.O., 2016. Corporate governance and risk management in the financial industry: changes after the global financial crisis.

Ortas, E., Gallego‐Alvarez, I. and Álvarez Etxeberria, I., 2015. Financial factors influencing the quality of corporate social responsibility and environmental management disclosure: A quantile regression approach. Corporate Social Responsibility and Environmental Management, 22(6), pp.362-380.

Wang, Z. and Sarkis, J., 2013. We are investigating the relationship of sustainable supply chain management with corporate financial performance. International Journal of Productivity and Performance Management, 62(8), pp.871-888.