SITHCCC005 Prepare Dishes Using Basic Methods of Cookery

February 22, 2023

A PROPOSAL FOR MANAGING CHANGE

February 25, 2023

Introduction

The financial market is a vital aspect of a nation’s economy since it has a direct impact on the prosperity of the nation on the global economic platform. It provides a platform where various parties are able to trade different financial assets including financial securities, stocks, bonds, etc. The market is mainly divided into various types. The first part is called the capital market and it mainly encompasses the stock market and bond market(Lee, Hutton & Shu, 2015). Other segments of the market are the money market, commodity market, spot market, and foreign exchange market. Since the market involves parties from different backgrounds, it is important to understand the underlying market concepts(Akbas et al., 2016).

Question 1

1a. Different levels of market efficiency

As per Cerutti, Dagher &Dell’Ariccia, market efficiency refers to the level to which the stock prices and various other securities prices reveal all the available and necessary facts and figures relating to the market and its operations. In simple words, an efficient can be described as a market that acts as a medium to transfer funds from the final lenders to the final borrowers in such a manner that this finance is used in an efficient manner and benefits one and all in the society. Eugene Fama was the economist who introduced the efficient market hypothesis (EMH) model which states that an investor can never outplay the market since all the available data and information is already included in the values of the stocks available in the market(Cerutti, Dagher & Dell’Ariccia, 2017).

So basically market efficiency determines the accessibility of market information so that maximum opportunities and scope is provided to the buyers and sellers who are involved in the transactions of various securities in the market without having to incur more transaction cost. A direct implication of an efficient market is that no specific investor or group of investors should be able to outperform the financial market by adopting a common strategy of investment(Cerutti, Dagher & Dell’Ariccia, 2017).

According to the efficient market hypothesis, there are various levels of market efficiency that are prevalent in the market namely weak-form efficiency, strong-form efficiency, and semi-strong efficiency.

- Weak-form efficiency

As per Chapple, Clarkson & Gold, the weak-form efficiency of the market implies that the market is efficient and all the market information relating to the historic prices is revealed in this form of market. Thus the movement of the future value cannot be determined by using the past prices and such former data are insignificant to predict the future stock price trend. Example – A is a broker who operates in the New York Stock Exchange. Recently he has been fascinated by investment and has no prior knowledge or experience with its operations and functioning(Chapple, Clarkson & Gold, 2013).

He observed that the price of XYZ gym equipment drops on Monday and increases on Friday. So on 1st May 2017, he bought 1000 shares of XYZ’s stock at $ 11 per share(Chordia et al., 2016). But on the coming Friday i.e 5th May 2017 he is very disappointed to observe that the prices of its shares have dropped to $ 10 per share. In this case, the market seems to be weak-form efficient since A was unable to earn an excess return by selecting his stocks based on past price trends.

- Strong-form efficiency

The strong-form efficiency of the market implies that the market is efficient and it reveals all the information which is both public and confidential in nature. Hence in this kind of market, no one can have an unfair advantage and predict prices to increase profits. There are no additional statistics available that can be used to increase the value of the investors(Cavusgil et al., 2014). Example – When corporate officials purchase their firm’s stock they need to intimate the government so that all the available data is made public so that their purchase transactions can become publicly known facts.

- Semi-strong efficiency

The semi-strong efficiency of the market implies that the market is efficient and it reflects all the publicly available facts and information. In this case, only the investors with inside and confidential information can have an advantage in the market scenario. Example – A held 100 shares of Medicine corp. which he had bought on 1st Han 2017 for $15 per share. The firm is involved in R&D activities concerning antibiotics. Since A is pretty experienced in the market, he does not check the market trend on a regular basis. The total outstanding shares of Medicine corp. were 3 million and he sold off his holding for $ 1200 (at $ 12) the very next day. By selling his shares in the firm, A was able to reduce his loss. But the very next day the firm’s stock price had increased to $ 13. This trend shows that the market was semi-strong form efficient since it had adjusted itself to the available information (Gopalan, Nanda & Seru, 2014).

1b. “Efficiency” of an emerging stock exchange market

According to Kristoufek & Vosvrda, the efficient market hypothesis (EMH) is one of the most vital concepts in finance subject. The efficiency of the market has vital implications for both the investors and the market authorities. If the market has an inefficient nature then the investors need to modify the market strategy in order to beat the market(Kristoufek & Vosvrda, 2014).

The authorities must try to restructure the market by applying effective laws and enhancing the financial media. If a market is efficient then the investors should focus on holding a well-diversified portfolio of financial devices. Investors that hold an inefficient diversified portfolio are prone to suffer losses since they are exposed to risk.

There are mainly two schools of thoughts about market efficiency. The first school argues that markets are efficient in form and hence the returns cannot be predicted or estimated in advance. This group supports the efficient market hypothesis model and state that price changes cannot be used to forecast future price trend.

As per Lavington, the second school on market efficiency focuses on the anomalies which could not be explained by the efficient market hypothesis model like the turn of the year effect which includes some stocks whose returns are very high in the initial few days of January month. The small firm effect refers to the tendency of undertakings with small market capitalization to surpass larger firms in the long run (Lavington, 2013). The day-of-the-week effect is the event in which the stock returns on Monday are lower as compared to other days of the week.

The various stock markets around the globe have different economic scenarios and legal implications with their specific government bodies. Some of the stock markets are developed markets, like the United States of America stock market, the United Kingdom stock market, and the Japanese stock market, which is liberal in nature. There are a few emerging financial markets like the Indonesian stock market, etc which have a number of restrictions(Lee, Hutton & Shu, 2015). The Chinese stock market has been analyzed to understand its efficiency form. Most scholars are of the view that the stock market of China is the weak form in nature. The Chinese stock exchange includes two official markets namely the Shanghai Stock Exchange (SSE), and Shenzhen Stock Exchange (SZE).

The features of the firms that are listed in the two markets are different. Most organizations that are listed on the SSE are large and state-owned whereas the firms listed on SZE are joint ventures, small, and mostly export-oriented(Lee, 2014). Since the Chinese market exhibits some peculiar ‘Chinese behavior’ a number of research activities have taken place. The literature on market efficiency and stock market predictability of China market is vast. A few methodologies have been adopted to test the efficiency form of the Chinese stock market. The activity adds value to the available literature by re-analyzing the weak form of the efficient market hypothesis by using the daily Chinese stock market data(Lam, 2014).

The data used to assess the “efficiency” of China’s stock exchange market is the daily closing price stock indices of the market in Shanghai and Shenzhen for A and B shares. The standard variance ratio VR test has been used for testing the market efficiency form. This method includes the random walk hypothesis and exploits the fact that the variance of this model’s increment is linear in nature in sampling intervals.

If “x” is a return generated from an asset in time “t” where “t” is 1,2,..,t. It is assumed that it is a result of the underlying stochastic process since it follows a martingale difference sequence. It explains that xt are uncorrelated but are conditionally or unconditionally random(López-Serrano et al., 2014). If the stock return adopts the random walk concept, the expected value of VR(x and k) will be equal to unity for all horizons k. And suppose the ratio is less than unity at the long horizon, then it indicates a negative serial correlation and if the ratio is more than unity at the long horizon, it implies a positive serial correlation.

A multiple VR test for joint null hypothesis i.e V(Ki) = 1 and i =1, ..,m for a holding period ki. This specific concept is based on the idea that a decision regarding the null hypothesis can be made on the basis of the maximum absolute value of the independent VR data. The data follows the studentized maximum model. The different VR findings suggest that institutional investors do not play any part in illustrating the results of weak-form efficiency tests. Foreign investors might have a disadvantage as compared to local investors due to reasons like the language barrier, different accounting principles, lack of necessary information, etc. Banks play an important role in the Chinese financial system but there is no connection between the relation between banks and the market and the efficiency of the Chinese stock market(Okonjo-Iweala, 2014).

Question 2

Capital market refers to an orderly market model which involves the effective and efficient transfer of financial resources from the investing audience to the entrepreneur group in both the private and public sectors of the economy. It is the market that mainly deals with long-term funds. It provides equity finance and long-term debt to the government body and other participants in the corporate sector. The various role and functions of the capital market are stated below:

Peirson et al said that the key role of the capital market is to mobilize financial resources and divert them into the productive channel. Thus it facilities and improves the economic condition of a nation. It acts as an important link between the saving class and the investing class. It transfers the financial resources from surplus sections to the deficit and productive areas and thus increasing the productivity of the nation(Peirson et al., 2014).

With the growth and development of the capital market, different banking and non-banking bodies provide various financial facilities which encourage people to save. In nations where there is a limited presence of a capital market, people hardly focus on saving money and the ones who save, put it in unproductive subjects and suffer losses.

Since the capital market provides lending facilities to various investors, it encourages investment. It offers different kinds of financial assets like shares, bonds, securities, etc to attract savers to lend or directly invest in the market. This market highlights the health of an economy and it accelerates the productive growth of a nation(Martinez & Philippon, 2014).

The investors have a number of benefits in this market since they are exposed to a healthy and marketable platform to perform investment transactions, their interest is ensured as they receive compensation from the stock exchange compensating fund in case of any fraudulent activity.

The money market is the segment of the financial market that deals with high liquidity and very short-maturity instruments. This platform is used by participants to borrow and lend in short-term financial assets, whose maturity period usually ranges from overnight to just less than a financial year. Some of the most typical money market instruments are commercial paper, municipal notes, treasury bills, etc. Generally, the transactions in this market take place between financial institutions and firms rather than individual investors.

Comment on the statutory and ethical consideration of a penetration tester working in the UK.

The crucial role and functions of the money market include financing ability in both international and internal trade activities(Martinez & Philippon, 2014). It encourages the growth of industries by providing them with short-term finance to meet their day-to-day capital requirements.

This market helps in the improved functioning of the capital market. The short-term interest rate offered in the money market influences the long-term interest rate charged in the capital market. It helps commercial banks to use the excess reserves in hand towards profitable investment activities. The existence of an efficient and developed money market helps in the better functioning of the central bank.

The money markets’ activities have an influence on the asset prices in the capital markets. Since the financial assets available in the money market of a financial market provide liquidity for the global financial system, they have a strong interrelation with the capital market, which makes up the financial market(Siegel, 2014). The capital market and its operations are affected by the nature and conditions prevailing in the money market.

The interest rate that is charged in the money market on its different financial resources has a bearing on the pattern of the interest rate charged in the capital market. This factor, in turn, affects the prices of financial assets that are available in the capital market of the economy. Thus the two parts of the financial market are closely related to each other.

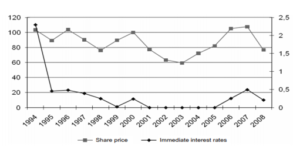

The particular scenario considered in the below graph relates to Japan’s financial market movement and the interrelation between the capital market and the money market. It shows that the interest rate charged in the money market has an impact on the share price in the capital market.

Figure 1: Share Price and overnight Interest rate development

Source: (Naveed, 2015)

The below graphical representation shows the share price pattern of Bharati Airtel Ltd which is a global telecommunications company based in India. It shows that its current share price is Rs 351.90 and there has been a 2.10% increase as compared to the former value. The data has been considered from March 17 to May 17 and it reveals that the share value of the firm was very high in March but then there was a decline phase on April 17(Peirson et al., 2014). The graphical model of the share movement helps to understand how the stock market keeps on fluctuating every moment.

Figure 2: Bharti Airtel Ltd. BSE Records

Source: (Okonjo-Iweala, 2014)

Question 3

3a. The nature of potential risks in international transactions

Risk refers to the uncertainties that might arise in the future. In the international trading scenario, the risk acts as a major barrier to the functioning and profitability in the trading background. The different kinds of risks and uncertainties that arise in the financial market include uncertainty, volatility, counterparty risk, interest rate risk, default risk, etc. The risk factor has a significant impact on the return of the investor on a both national and global level. When the project life increases, the uncertainty relating to its operations also increases(Peirson et al., 2014).

The market risk basically is the possibility for an investor to suffer some kind of loss due to a number of factors that affect the overall performance of the financial market in which he operates. The market risk cannot be stopped by diversification but it can be hedged against. The two major categories of investment risk are known as market risk and specific risk. Market risk arises due to external factors over which a firm has no control(Martinez & Philippon, 2014). Specific risk relates to a certain set of firms. The different kinds of risks in international trade have been elaborated on below:

Volatility – It is a crucial risk that is prevalent in most markets. It refers to the uncertainty which arises regarding the change in the value of a particular asset. There are various kinds of statistical measures that have defined the historical volatility of a given asset. When the level of volatility is higher it means that a larger movement or change in the value of the financial asset(Lam, 2014). An asset that has a higher chance of fluctuation in its value has a positive chance of moving up just like it has a chance that its value will go down. Such assets have a significant impact on the value of the investor’s portfolio.

http://cheapestassignment.com/cmu201-business-communications/

Exchange rate risk – It is a crucial risk which affects the profit or loss of an investor who performs trade at an international level. The unfavorable movement of the exchange rate reduces the profit of the party. If the party opts to lock in the exchange rate then it forfeits the opportunity of earning profit from the favorable movement of the exchange rate.

Counterparty risk – This particular risk is mainly associated with the derivative swap market. It arises when one of the parties in an agreement is involved in a credit swap. The term

Credit swap refers to the exchange of cash flow between two factions and it is based on the movement that takes place in the underlying interest rate.

Default risk – This risk happens in the bond and fixed-income markets. This risk arises when there is a possibility that a borrower may default on his loan obligations and the lender might suffer losses since he will not receive the outstanding amount(Kristoufek & Vosvrda, 2014).

Interest rate risk – This risk also arises in the bond market which occurs when the value or price of the bonds decreases with the increase in the interest rate figure.

Hence investors need to thoroughly analyze the risk and reward aspects before performing any kind of investment-related transaction in the financial market on a national and international platform.

International traders need to manage such kinds of risks to have the minimum impact on exchange rate risk in the forward foreign exchange market, the party might decide to lock in the exchange rate at the value at which the currency was bought. Hedging is an important concept that helps investors to eliminate market risk. Example – Hedging credit can help protect against increasing interest rates. Firms can increase the role of IT systems to study the pattern of market risk and prepare themselves to minimize their losses.

Spot contract refers to the contract which involves the sale or purchase of a commodity, security, or currency for prompt delivery and payment on the spot date, i.e normally two business days after the trading took place. Spot rate refers to the price that is quoted for the instantaneous settlement of the particular spot contract. Hence a spot foreign exchange rate refers to the figure of a foreign exchange contract that has been arrived at for immediate delivery which takes place generally within two days(Chapple, Clarkson & Gold, 2013).

The spot rate shows the price or value that the purchaser is willing to sacrifice for a foreign currency in terms of a different currency. Mostly these contracts are used for immediate transactions. Example – property purchases, deposits on cards, etc. Various investors can also opt to purchase a spot contract to lock in an exchange rate through a particular future date.

http://cheapestassignment.com/hi5019-strategic-information-systems-trimester-3/

Forward foreign exchange refers to a contract in which a certain sum of foreign currency is bought and sold for a specific value for the settlement at a pre-agreed future date or within a particular range of fixed future dates. Such kinds of contracts can be used to lock in the currency rate so that an unfavorable movement in the future can be curtailed by the involved party. In simple terms, this kind of contract can be explained as an agreement of contract terms on a current date with the delivery and payment on a specified future date. Depending on the security that is being traded, the forward rate can be arrived at by using the spot rate.

The main advantage of the spot and the forward foreign exchange is that it helps in the efficient management of market risk. It allows the involved party to protect the cost of the products and services that are purchased beforehand, it also helps to shield the profit margin that is sold abroad(Chapple, Clarkson & Gold, 2013).

If the exchange rate is locked-in for as long as a year in advance, it enables the party to avoid the risk associated with currency fluctuation, which is also known as currency hedging.

Question 4

Asymmetric information – Asymmetric information refers to the situation when one particular party involved in an economic transaction has more access to material knowledge and information as compared to the other party. It is also termed information failure. This kind of situation generally arises in the case of sale and purchase situations when a seller of a product or service has greater knowledge than the purchaser. In multiple economic transactions, such information asymmetries take place. In some circumstances, asymmetric information may hurt the operations involved in economic activity(Cerutti, Dagher & Dell’Ariccia, 2017).

This information failure mainly arises where the information involved is complex in nature. The customer might be at the receiving end due to such a problem, so financial markets mainly rely on the reputation mechanism to prevent the exploitation of consumers or clients.

The financial analysts and advisors that have a reputation to be the most trustworthy and effective stewards of their client’s assets tend to get several clients, while the fraudulent or ineffective firms lose clients or face legal issues. Example – While selling an automobile, the seller has full knowledge about the product but the potential buyer is unaware of several features of the automobile(Akbas et al., 2016).

Moral hazard – The issue relating to moral hazard arises when one party to an economic transaction has not entered the specific activity with good intentions. He might share misleading details about his firm’s operations, assets, liabilities, etc. Moral hazard can occur at any point in time when two associations agree. Both parties will have the opportunity to have an unfair gain by not abiding by the rules and principles laid down in the agreement(Cavusgil et al., 2014).

Generally, this concern takes place when one party gets the scope to assume the extra risk that negatively impacts the other party. Since the main criteria in such an event are related to the decision or choice which is considered to be right, the reference to morality is given. It could apply to the functioning of the financial sector. Example –Contract between a borrowing party and money lender.

Adverse selection – In the economic concept, adverse selection refers to the particular scenario where the seller has more details concerning the product and its features than the purchaser, or vice versa. In simple words, this can be explained as the case when one party in dealing has more necessary information than the other party. Such circumstances lead to bad decision-making processes and might affect the profitability of a firm.

The traders who have access to better information will selectively and carefully participate in a trade to earn excess profits. Example – A firm’s stocks will be bought by its managers who are aware of the trend of the current stock value(Cavusgil et al., 2014).

Since different kinds of situations might occur in the financial market, it is necessary to regulate financial markets. The proper and efficient regulation of the financial market acts as a framework that minimizes such issues as moral hazard, adverse selection, and asymmetric information flow. It helps in maintaining the integrity of financial transactions. Financial stability and consumer protection are the direct impacts of having a properly regulated financial market in a nation.

Conclusion

The financial market topic is vast since it includes various sub—markets which have specific methods of operation. It is necessary to understand the different elements that play a vital role in the efficiency of the financial market. The role and link between the capital market and the money market have been highlighted which shows how various activities are interlinked in the huge market. The different kinds of risks that affect the rewards of the involved parties have been analyzed to understand the methods that can be adopted to minimize such risks.

References

Akbas, F., Armstrong, W.J., Sorescu, S. and Subrahmanyam, A., 2016. Capital market efficiency and arbitrage efficacy. Journal of Financial and Quantitative Analysis, 51(02), pp.387-413.

Cerutti, E., Dagher, J. and Dell’Ariccia, G., 2017. Housing finance and real-estate booms: a cross-country perspective. Journal of Housing Economics.

Chordia, T., Subrahmanyam, A. and Tong, Q., 2014. Have capital market anomalies attenuated in the recent era of high liquidity and trading activity? Journal of Accounting and Economics, 58(1), pp.41-58.

Chapple, L., Clarkson, P.M. and Gold, D.L., 2013. The cost of carbon: Capital market effects of the proposed emission trading scheme (ETS). Abacus, 49(1), pp.1-33.

Chordia, T., Goyal, A., Nozawa, Y., Subrahmanyam, A. and Tong, Q., 2016. Are capital market anomalies common to equity and corporate bond markets? An empirical investigation.

Cavusgil, S.T., Knight, G., Riesenberger, J.R., Rammal, H.G. and Rose, E.L., 2014. International business. Pearson Australia.

Gopalan, R., Nanda, V. and Seru, A., 2014. Internal capital market and dividend policies: Evidence from business groups. Review of Financial Studies, 27(4), pp.1102-1142.

Kristoufek, L. and Vosvrda, M., 2014. Measuring capital market efficiency: long-term memory, fractal dimension, and approximate entropy. The European Physical Journal B, 87(7), p.162.

Lavington, F., 2013. The English capital market. Routledge.

Lee, L.F., Hutton, A.P. and Shu, S., 2015. The role of social media in the capital market: evidence from consumer product recalls. Journal of Accounting Research, 53(2), pp.367-404.

Lee, J.W., 2014. Will the Renminbi Emerge as an International Reserve Currency? The World Economy, 37(1), pp.42-62.

Lam, J., 2014. Enterprise risk management: from incentives to controls. John Wiley & Sons.

López-Serrano, A., Olivas, R.M., Landaluze, J.S. and Cámara, C., 2014. Nanoparticles: a global vision. Characterization, separation, and quantification methods. Potential environmental and health impact. Analytical Methods, 6(1), pp.38-56.

Okonjo-Iweala, N., 2014. Unleashing the housing sector in Nigeria and Africa. In 6th Global Housing Finance Conference.

Peirson, G., Brown, R., Easton, S. and Howard, P., 2014. Business finance. McGraw-Hill Education Australia.

Martinez, J. and Philippon, T., 2014. Does a currency union need a capital market union? Working Paper, NYU.

Naveed, M., 2015. The Size of the Islamic Finance Market. Retrieved May, 28, p.2015.

Siegel, J.J., 2014. Stocks for the Long Run 5/E: The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies: The Definitive Guide to Financial Market Returns & Long-Term Investment Strategies (EBOOK). McGraw Hill Professional.